SEJONG -- A large proportion of middle-aged South Koreans have become hugely indebted to financial firms over the past few years due to their apartment purchases.

The previous Park Geun-hye administration provided them with relaxed loan terms in a bid to induce as many households as possible to purchase apartments, a policy aimed at boosting the economy.

More recently, younger people in their 20s and 30s have joined the move, a lawmaker has reported.

Those, who have bought homes in Seoul in the two age groups, took out mortgages worth about 300 million won ($256,000) on average. And the average prices of their housing units were 480 million won for those in their 20s and 550 million won in their 30s.

Some market insiders say that many of them, those in their 20s in particular, could have been supported by their parents in their property purchases, while online commenters cast doubt over young people’s financial capacity.

Despite their substantial mortgages, those who bought homes in Seoul during the previous Park administration (2013-2017) are regarded as “winners” at the current stage, because apartment prices in the capital have soared by about 50 percent, and up to 100 percent in some cases, since President Moon Jae-in began his term in May 2017.

|

Information on prices of apartment units, put up for sale, are posted on the window of a real-estate agent office in Seoul earlier this year. (Yonhap) |

On the other hand, the huge sum of outstanding household loans, involving mortgages, has been a core factor hampering consumption in the household sector and macro-economic growth.

Despite the spike in their home prices, ordinary households -- owning only one apartment unit and indebted to commercial banks – inevitably have their ability to spend restricted due to debt repayment burdens, unless they choose to realize capital gains by selling their homes and moving to cheaper areas.

Further, a certain portion of households in provincial cities saw their apartment prices fall after purchasing them, which is aggravating risks to those indebted to financial firms.

This situation means that ordinary Koreans lack flexibility in their spending abilities, compared to households of foreign major countries.

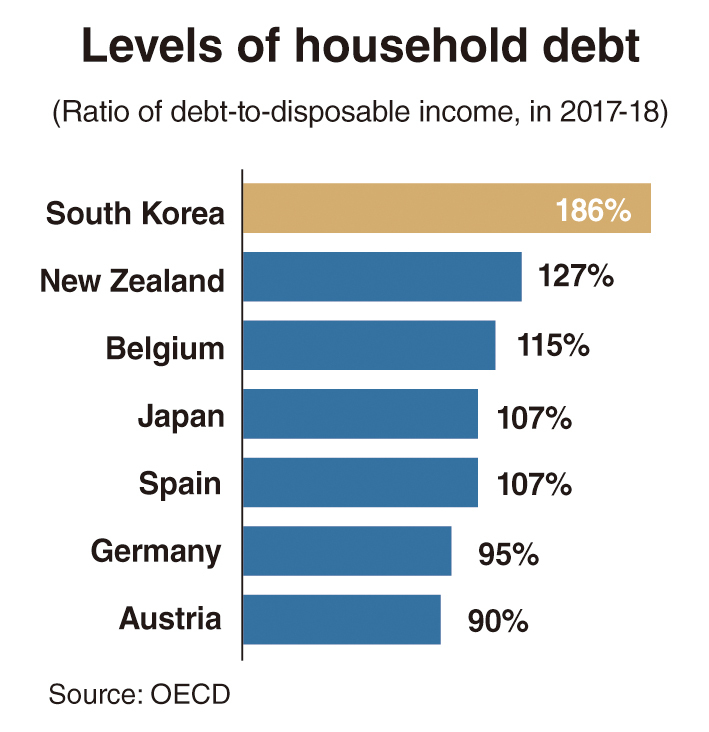

The Organization for Economic Cooperation and Development has compared the ratio of household debt to net disposable income among 32 out of its 36 members, based on their 2018 or 2017 data. Four -- Iceland, Israel, Mexico and Turkey -- were not included in the research.

South Korea had an average household debt-to-disposable income ratio of 186 percent, which was the eighth-highest among the 32 countries.

Korea lagged behind major economies in the household financial soundness. The figures were 146 percent in the UK, 120 percent in France, 109 percent in the US, 107 percent in Japan, 95 percent in Germany and 87 percent in Italy.

The level was more serious than in emerging economies in the OECD -- Estonia with 80 percent, Slovakia with 79 percent, Chile with 70 percent, the Czech Republic with 70 percent, Poland with 62 percent, Slovenia with 57 percent, Lithuania with 50 percent, Latvia with 42 percent and Hungary with 42 percent.

A ratio under 100 percent could be seen as indicating quite strong financial soundness in the household sector and a low possibility of loan-insolvency for financial firms.

|

(Graphic by Yoon Jeong-soon/The Korea Herald) |

Only seven countries had higher ratios than South Korea -- Luxembourg, Sweden, Switzerland, Australia, Norway, Netherlands and Denmark. But all of the seven had higher per capita national income than Korea, and their governments offer better social welfare conditions.

Korean households have seen the debt-to-disposable income ratio continue to rise over the past decade to surpass the 180 percent mark since 2016, compared to about 150 percent in 2010.

It is heading toward 200 percent, which indicates that debt doubles their disposable income.

The OECD has specified that the debt in the members’ comparison is calculated as the sum of the liability categories: loans -- primarily mortgage loans and consumer credit -- and accounts payable.

According to financial market insiders, Korea’s outstanding loans to households are estimated to have exceeded 2 quadrillion won, when the data includes the 600 trillion won of loans extended to the self-employed.

The Bank of Korea has been supportive in government policies to boost GDP growth by letting the benchmark interest rate stay under 2 percent for more than four years since March 2015, which has triggered a full-fledged rush to the property market amid record-low rates: it is set at 1.25 percent per annum.

But the National Assembly Budget Office has warned a possibly sliding GDP growth and private consumption from a rising household-debt balance.

By Kim Yon-se (

kys@heraldcorp.com)

![[Herald Interview] 'Trump will use tariffs as first line of defense for American manufacturing'](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/11/26/20241126050017_0.jpg)

![[Health and care] Getting cancer young: Why cancer isn’t just an older person’s battle](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/11/26/20241126050043_0.jpg)

![[Graphic News] International marriages on rise in Korea](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/11/25/20241125050091_0.gif)