This is the 38th in a series of articles analyzing major companies traded on the tech-heavy Kosdaq market. – Ed

CJ O Shopping, a leading home-shopping channel in South Korea, is likely to benefit from recovering consumers’ sentiment as the country is set to hold the presidential election in May, as well as an overall improvement in its competitiveness analysts here predicted.

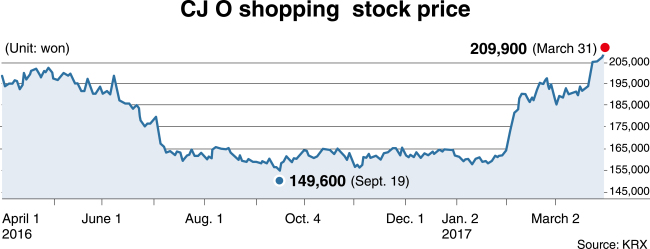

Shares in CJ O Shopping, the 12th largest on the tech-heavy Kosdaq market in terms of market capitalization with 1.3 trillion won ($1.16 billion) as of Friday, remained sluggish last year hurt by weak consumers’ sentiment amid a political scandal that rocked the country for months and led to the impeachment of former President Park Geun-hye.

The company has also been hit by a row with China over the deployment of the US-backed missile defense system due to its exposure to the Chinese market. In recent years, the home-shopping channel has expanded its presence in the world‘s second largest economy in an attempt to target China’s burgeoning e-commerce market. CJ O Shopping has a stake in its Chinese subsidies -- Dongfang CJ, Tiantian CJ and Nanfang CJ.

Analysts said the home-shopping channels overall are likely to enjoy a recent recovery in consumers’ sentiment and the presidential election set to be held on May 9. The composite consumer sentiment index compiled by the Bank of Korea improved for two consecutive months after hitting the lowest level in nearly eight years in January.

Historically, consumers’ sentiment was boosted after three presidential elections in 2002, 2007 and 2012, according to Yu Jung-hyun, an analyst at Daishin Securities.

Samsung Securities analyst Nam Ok-jin said in his report last month that while CJ O Shopping suffered dull growth from the second half of 2014 to the first half of last year due to botched mobile marketing strategies and lowered product competitiveness, it has been posting large operational profit since the second half of last year.

The company‘s operation profit came at 144.9 billion won last year, the largest in the business.

“The company’s total market price comes at around 1.2 trillion won, which is slightly lower compared to about 1.4 trillion won of its rivals. Based on recent changes, the price of CJ O Shopping will increase the largest,” Nam said.

He cited how the previous “discount factors” such as its weak overseas sales and failed sales of its CJ Hellovision are starting to be resolved, such as new potential buyers for CJ Hellovision emerging.

The company is also expected to recover its product competitiveness by reducing the lineup of low-margin products, while continuing to enjoy smooth revenue from retail services.

The company will also enjoy reduced competition with online shopping companies, and see sales growth for the TV channel, Daishin and Shinhan Investment Corp both said in separate reports last week.

CJ O Shopping is expected to post a gross sales of 794.4 billion won in the first quarter of this year, up 7.7 percent on-year, and an operating profit of 38.2 billion won, growing 5.5 percent on-year, according to Shinhan, which has set its target price of 240,000 won for CJ O Shopping.

“The company’s price-earning (P/E) ratio is just 10.9 despite over a 20 percent rise in the share price during this year,” Shinhan analysts Park Hee-jin and Kim Kyu-ri wrote in a report. This is a lower valuation versus peers such as GS Home Shopping whose P/E ratio is 12.7.

Increase in gross sales of the TV channel and lower transmission fee hike would also give a boost to the company’s share price, they added.

On Friday, shares in the firm closed at 209,400 won, up 1.55 percent from the previous day.

By Park Ga-young (

gypark@heraldcorp.com)

![[Herald Interview] 'Korea, don't repeat Hong Kong's mistakes on foreign caregivers'](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/11/13/20241113050481_0.jpg)

![[KH Explains] Why Yoon golfing is so controversial](http://res.heraldm.com/phpwas/restmb_idxmake.php?idx=644&simg=/content/image/2024/11/13/20241113050608_0.jpg)